Australia’s Insurance Protection Gap Is a Property Data Problem

APRA’s 2026 ICVA results, and what they mean for insurance pricing, mortgage risk and land use planning.

Australia’s home insurance market is under growing pressure. More frequent extreme weather events have pushed claims costs higher, and premiums have followed. For a rising number of households, the cost of maintaining adequate cover has become difficult to absorb, and many have reduced or dropped it altogether.

The Australian Prudential Regulation Authority (APRA) is the federal body that oversees Australia’s banks, insurers and superannuation funds. In March 2026 it published its most detailed assessment of where this trend is heading, through its Insurance Climate Vulnerability Assessment (ICVA). The findings are significant.

Around one in seven Australian homes is uninsured today. Under both of APRA’s stress scenarios, that figure rises to around one in four by 2050. That is one million additional properties losing cover, at roughly 40,000 homes each year.

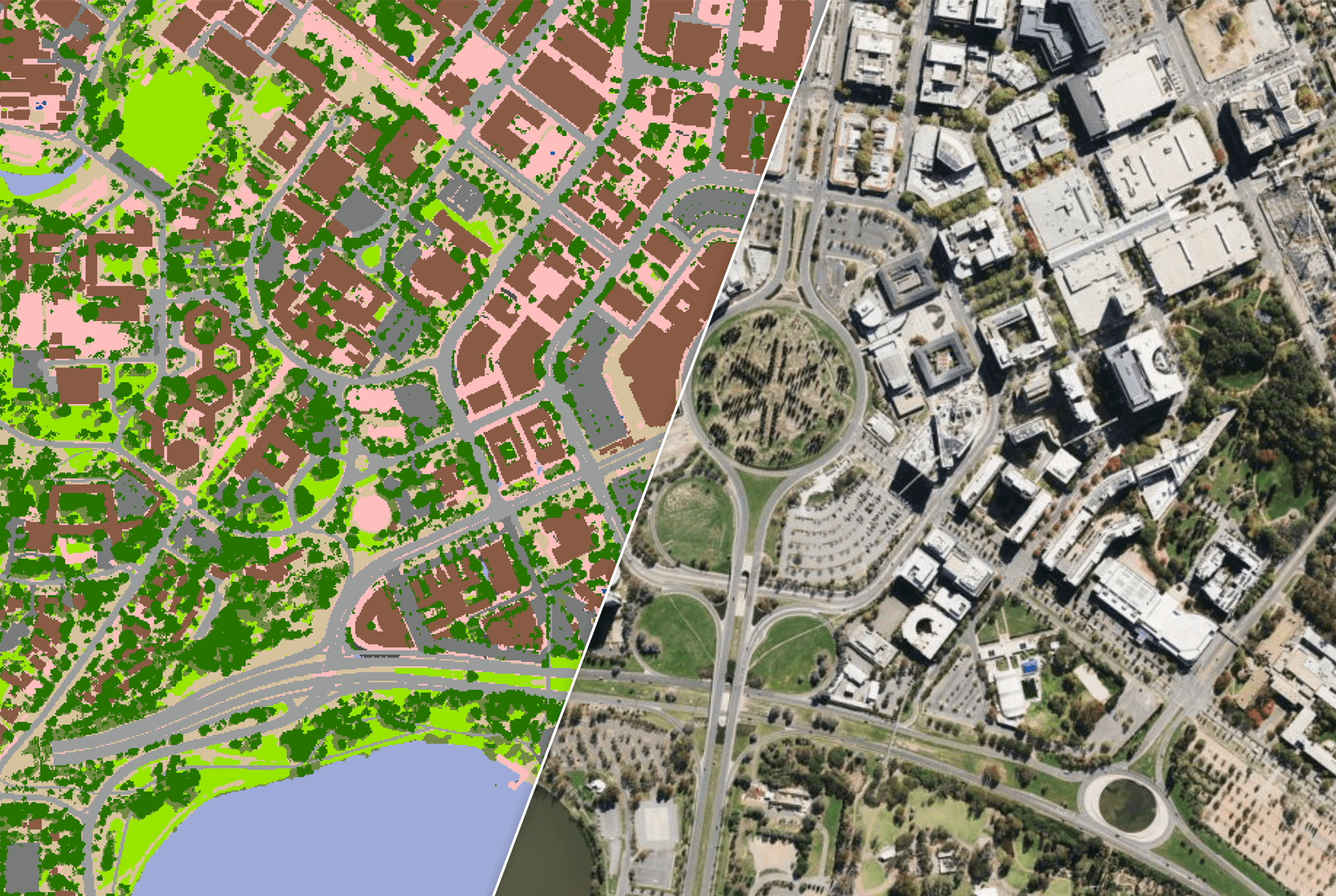

APRA calls the shortfall between what disasters cost and what insurance covers the protection gap. The ICVA is the most comprehensive stress test of how that gap could widen under different climate futures. Geoscape provided the national property dataset that underpinned its modelling. You can read more about that work here.

The challenge

The protection gap widens when households drop insurance because premiums become unaffordable. When enough households do the same, it stops being a personal finance problem and becomes a risk to the financial system.

APRA modelled two pathways through which climate change accelerates that process.

Under the higher physical risk scenario, more frequent and severe weather events push expected annual losses from around $7 billion today to more than $16 billion by 2050. Higher claims costs drive premiums up. As premiums rise, households drop cover.

Under the higher transition risk scenario, construction cost inflation drives premiums up even where physical losses are less severe. The cost of rebuilding a home rises, and so does the cost of insuring one.

Both pathways produce the same result. Premiums outpace household incomes and the insured pool shrinks.

Who bears the most exposure

- Regional and rural communities, where over 40 per cent of rural households could be uninsured by 2050 under both scenarios

- Communities with lower average incomes, where premium increases are harder to absorb

- Banks holding uninsured mortgage collateral, as most lenders do not verify cover is maintained over the life of a loan

- 180,000 mortgage-holding households already facing insurance affordability stress, representing $57 billion in loan balances

Where location intelligence fits

The protection gap widens when risk is priced too broadly. Risk priced at broad geographic levels can still miss meaningful property-level differences. A household on elevated ground near a floodplain may face the same flood premium as a house at grade in the same postcode. Lower-risk households end up overpaying. Some drop cover.

When lower-risk properties leave the insured pool, the concentration of risk behind them grows. The ICVA points to three areas where property-level data can change that dynamic.

Insurance pricing

Flood risk varies significantly at the property level. Two houses in the same postcode can carry very different exposure depending on their elevation relative to surrounding terrain.

Pricing that cannot distinguish between them will misprice both.

First Floor Elevation data captures building-level elevation across Australia, giving insurers the granularity to reflect actual property risk.

Mortgage collateral and the insurance register

Most lenders require home insurance as a mortgage condition but have no mechanism to verify that cover remains in place over the life of a loan.

APRA has proposed a centralised insurance register to close that gap. Building such a register requires a consistent spatial layer connecting insurance records to physical properties at a national scale.

The National Buildings Dataset provides that foundation.

Risk-based land use planning

Development decisions made today determine the risk profile of Australia’s housing stock for decades.

Assessing climate exposure at the property level before land is committed gives planners and regulators the basis for decisions that account for long-term insurability, not just current hazard maps.

What the sector does next

APRA is clear that the ICVA is a stress test. The one-in-four figure represents a modelled scenario under sustained pressure, not a fixed outcome. But the conditions driving it are already present, and the data needed to respond already exists. The question is how quickly insurers, banks and planners build it into their risk frameworks before the protection gap becomes significantly harder to close.